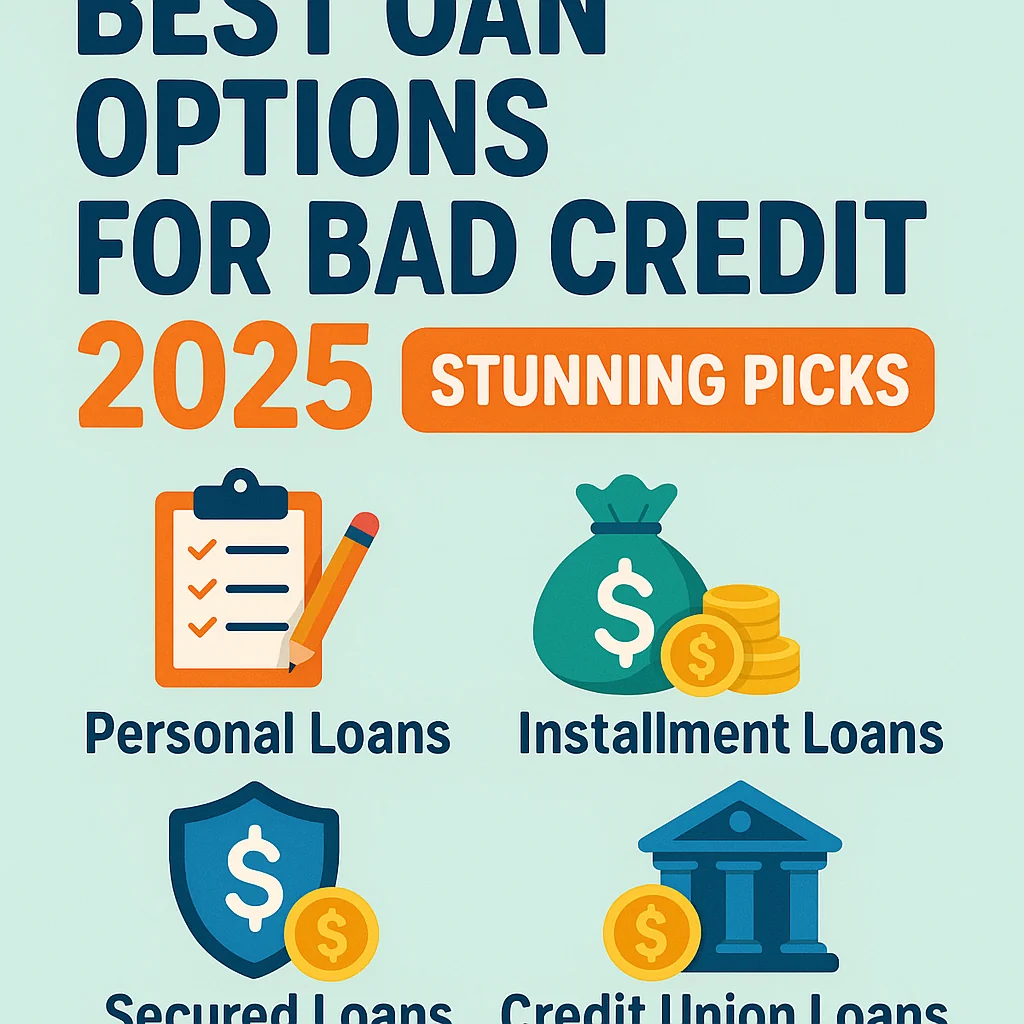

Best Loan Options for Bad Credit 2025: Stunning Picks.

Article Structure

Bad credit does not close every door. It changes your options and your costs, but you can still borrow money in 2025 if you know where to look and what to avoid. The key is to compare offers carefully and protect yourself from very expensive debt.

What “Bad Credit” Means in 2025

Most lenders still use a 300–850 credit score range. Scores under 580 usually count as poor, and scores between 580 and 669 are often seen as fair. With poor or fair credit, you can get approved, but you face higher interest rates, stricter limits, and more checks on your income and spending.

Imagine two people applying for the same $5,000 loan. One has a 750 score, the other has a 540 score. The first might pay a single-digit interest rate and finish the loan fast. The second might pay two or three times as much interest and struggle to keep the payment under control. That gap is what you need to manage.

Main Loan Options for Bad Credit Borrowers

People with bad credit in 2025 usually choose from a small group of loan types. Each one has its own rules, risk level, and price tag. The best choice depends on your income, assets, and how fast you need the money.

1. Secured Personal Loans

Secured personal loans use something you own as collateral. Lenders may accept a car, savings account, fixed deposit, or other assets. Because the lender can claim the collateral if you do not pay, the interest rate is often lower than on unsecured loans for the same credit score.

For example, a person with a weak score might struggle to get an unsecured $4,000 loan, but could be approved for the same amount if they back it with a paid-off car worth $6,000. The risk is clear: miss too many payments, lose the car.

2. Unsecured Bad Credit Personal Loans

Unsecured bad credit loans do not need collateral. Lenders base approval on your credit history, income, and debt-to-income ratio instead. These loans are easier to get than prime loans, but the price is high. APRs can range from the mid-teens up to 36% or more, depending on your country and lending laws.

This option can be useful for emergency costs like medical bills or urgent repairs. Still, it works best when you keep the loan amount small and the term short to limit interest costs.

3. Credit Union and Cooperative Loans

Credit unions, cooperatives, and community lenders often treat bad credit more softly than large banks. They look at your history with the group, your savings habits, and your current income. In many cases they cap interest rates and avoid aggressive fees.

Someone with a 560 score who has saved regularly in a cooperative account for two years might still get a decent offer. It might not be cheap, but it can be far less punishing than a payday or online high-interest loan.

4. Buy Now, Pay Later (BNPL) and Point-of-Sale Financing

In 2025, many stores and online platforms offer BNPL plans. Some do a soft credit check, others rely more on your recent payment history with them. These options break a purchase into several fixed payments and often charge low or zero interest if you pay on time.

The trap comes if you miss payments or stack too many plans at once. Late fees and penalty rates can build up. BNPL works best for one clear purchase that fits into your monthly budget without strain.

5. Secured Credit Cards and “Second-Chance” Cards

While not a traditional loan, secured credit cards and some “second-chance” cards are practical tools for people with bad credit. You pay a security deposit, which becomes your credit limit. Use the card, pay in full each month, and the issuer reports your good behavior to credit bureaus.

Over 12–18 months, this pattern can help move you out of the high-risk group. That opens doors to cheaper loans later. This choice suits people who need a small line of credit and want to rebuild, not those who need a big sum in one go.

6. Peer-to-Peer and Online Marketplace Loans

Peer-to-peer platforms match borrowers with individual or institutional investors. Some of these platforms accept bad credit borrowers but charge more interest and may require extra proof of income or a co-borrower.

The upside is speed and simple online applications. Some people receive a decision in hours. The downside is that fees and rates can be high if your score is low. Always check the APR, not just the monthly payment.

Loan Types to Treat With Extreme Caution

Loans exist that target people with bad credit because they are easy to sell. Many of these products cost far more than they seem at first glance. Careful review of the fine print is essential.

Payday Loans

Payday loans offer small sums due on your next paycheck. They often use flat fees instead of clear APRs. When you convert the fee into an annual rate, it can reach several hundred percent. Many borrowers cannot pay the loan in full on the due date, so they roll it over and pay more fees again and again.

This cycle can turn a $200 shortfall into a long-term money drain. If you are already under pressure, payday loans can pull you deeper into debt.

Auto Title Loans

Auto title loans use your vehicle as collateral. The lender holds your car title and you keep driving the vehicle. These loans are usually short-term and very expensive. Miss enough payments and you can lose the car, even if you already paid off most of the loan amount.

For many people, a car is needed for work and daily life. Losing it can damage both income and stability, so title loans sit at the high-risk end of the borrowing range.

Comparison of Common Bad Credit Loan Options

The table below gives a rough idea of typical features for popular bad credit loan options in 2025. Exact numbers depend on your country, lender, and personal profile, but the pattern stays similar across markets.

| Loan Type | Needs Collateral? | Typical APR Range | Best Use Case | Main Risk |

|---|---|---|---|---|

| Secured personal loan | Yes | 8%–25% | Larger expenses, debt consolidation | Losing the asset if you default |

| Unsecured bad credit loan | No | 18%–36% | Urgent cash needs | High interest and long-term debt |

| Credit union / cooperative loan | Often no | 10%–28% | Members with weak scores but stable income | Limited loan amounts |

| BNPL / POS financing | No | 0%–30% | Specific purchase at checkout | Late fees and multiple open plans |

| Payday loan | No | 200%+ equivalent | Short-term small gaps (last resort) | Debt rollover and fee spiral |

APR ranges are indicative, not exact, and vary by country, regulation, and lender type.

How to Choose the Best Bad Credit Loan for Your Situation

The “best” loan for bad credit is not the one with the biggest approval rate. It is the one that solves your problem with the least damage to your future budget. A simple decision process can help you sort options fast.

- Define the exact amount you need and why you need it.

- Check if you can cut or delay some costs instead of borrowing.

- List assets or savings that you are willing to use as collateral.

- Compare offers from at least three different lender types.

- Run the numbers on total interest and fees, not only the monthly payment.

Use a loan calculator or a simple spreadsheet. Enter the loan amount, rate, and term, then look at the total paid back. If you borrow $3,000 at 28% for three years, the final cost can shock you. That shock is useful. It shows whether the loan solves your problem or just postpones it.

Practical Tips to Improve Approval Odds in 2025

A bad credit score is not the only factor lenders review. You can improve your odds and your pricing by making a few smart moves before you apply. Even two or three small changes can help.

- Pay down high credit card balances a bit before you apply to lower your credit utilization.

- Settle or bring current at least one overdue account, if possible.

- Gather proof of stable income, such as payslips, tax returns, or client invoices.

- Add a co-signer with better credit if you fully trust each other.

- Choose a shorter term if you can handle the higher payment, since lenders see that as lower risk.

Imagine you clear a small $200 past-due bill and reduce a credit card from 90% used to 60% used. Your score may move more than you expect. Even a jump of 20–30 points can move you into a bracket with better rates or faster approvals.

Red Flags and Scams to Avoid

People with bad credit are common targets for scams or very unfair offers. A little skepticism saves money and trouble. If an offer looks too easy, slow down and inspect it.

Watch out for lenders that promise guaranteed approval without any credit or income check. Also avoid companies that ask for large up-front “processing fees” before you receive the loan, especially if payment is requested through gift cards or crypto. Trustworthy lenders earn money from interest and clear fees that are paid over the life of the loan, not from secret charges before approval.

Short-Term Fix vs. Long-Term Strategy

Using a loan to cover a one-time emergency can be reasonable. Using new loans to pay old loans month after month is a warning sign. If your problem is ongoing cash flow, not a one-off shock, the real fix lies in your budget, not in the next lender on your list.

A smart plan in 2025 might include three steps at once: a small, clearly structured loan; a spending review to cut non-essential costs; and a focused credit rebuild effort through on-time payments. Over a year or two, that mix reduces your reliance on expensive bad credit products and opens access to far cheaper money.

Key Takeaways for Borrowers With Bad Credit

Bad credit limits your options, but it does not erase them. Secured personal loans, credit union loans, and certain online personal loans can still be useful if you compare offers and keep the amount and term under control. Payday and auto title loans sit at the last-resort end of the spectrum because of their extreme costs and high risk.

The best loan option is the one you can repay comfortably, with clear terms, fair pricing, and no hidden traps. Treat each offer with a cool head, check the total cost, and give yourself time to rebuild your credit so that the next loan you need in the future is cheaper and easier to handle.