Paycheck Advance vs Payday Loans: Stunning Best Guide.

Article Structure

Understanding how each option works, how much they cost, and what can go wrong helps you choose the lesser risk or even avoid both.

What Is a Paycheck Advance?

A paycheck advance is early access to money you have already earned but have not yet received as a paycheck. It is usually smaller, linked to your salary, and often repaid on your next pay date.

This type of advance can come from three main sources: your employer, a bank or app, or a credit union. Each source has different rules and costs.

Employer-Based Paycheck Advances

Some employers let staff request a portion of their upcoming paycheck before the official payday. This might be called an “earned wage access” program, salary advance, or payroll advance.

Example: You earn $2,000 per month and get paid on the 30th. On the 20th, you ask HR for a $300 advance. The company sends you $300, and on the 30th your paycheck is $1,700 instead of $2,000.

- The advance is limited by your expected earnings.

- Repayment is usually through automatic payroll deduction.

- Some employers offer this free; others charge a small flat fee.

Employer options tend to be cheaper than loans because they are tied to your job, not your credit score.

Bank or App-Based Paycheck Advances

Some banks, fintech apps, and digital wallets now offer “early wage access” or “cash advance” features. They review your direct deposit history and allow you to access a part of your estimated pay before it arrives.

Example: A banking app sees your last six paychecks land on the 15th. On the 10th, it offers you up to $150 as an advance against your next paycheck, which will be taken back when the deposit lands.

These services often work like this:

- You connect your salary account or upload pay stubs.

- The app estimates your upcoming pay and sets a limit.

- You request an advance, usually under a set cap (for example, up to 50% of earned wages or a fixed dollar limit).

- The app withdraws the advance on payday automatically.

Many apps advertise “no interest”, but they may charge subscription fees, instant transfer fees, or ask for “tips”. These costs can add up if you use the service often.

What Is a Payday Loan?

A payday loan is a short-term, high-cost loan that is due in full on your next payday or within a few weeks. The lender is usually a payday store, an online lender, or a small credit company, not your employer.

The key point: payday loans are new debt. They are not based on wages you already earned. The lender expects you to repay the full amount plus a fee, often by giving them access to your bank account or a post-dated check.

How Payday Loans Work in Practice

Imagine you borrow $300 from a payday lender with a fee of $45, due in 14 days. On your next payday, the lender attempts to pull $345 from your account. If you do not have the money, the lender can roll the loan into a new one with another fee.

The fees may not look huge in isolation, but the effective annual percentage rate (APR) is often extremely high. Many payday loans work out to triple-digit APRs once you convert the fees to an annual rate.

- Short terms: usually 7–30 days.

- High fees: often a flat fee per $100 borrowed.

- Automatic repayment: post-dated check or bank access.

- High risk of repeat borrowing and a debt spiral.

For many borrowers, paying back the full amount plus fees in one shot is hard, which leads to rolling the loan over and paying more fees each cycle.

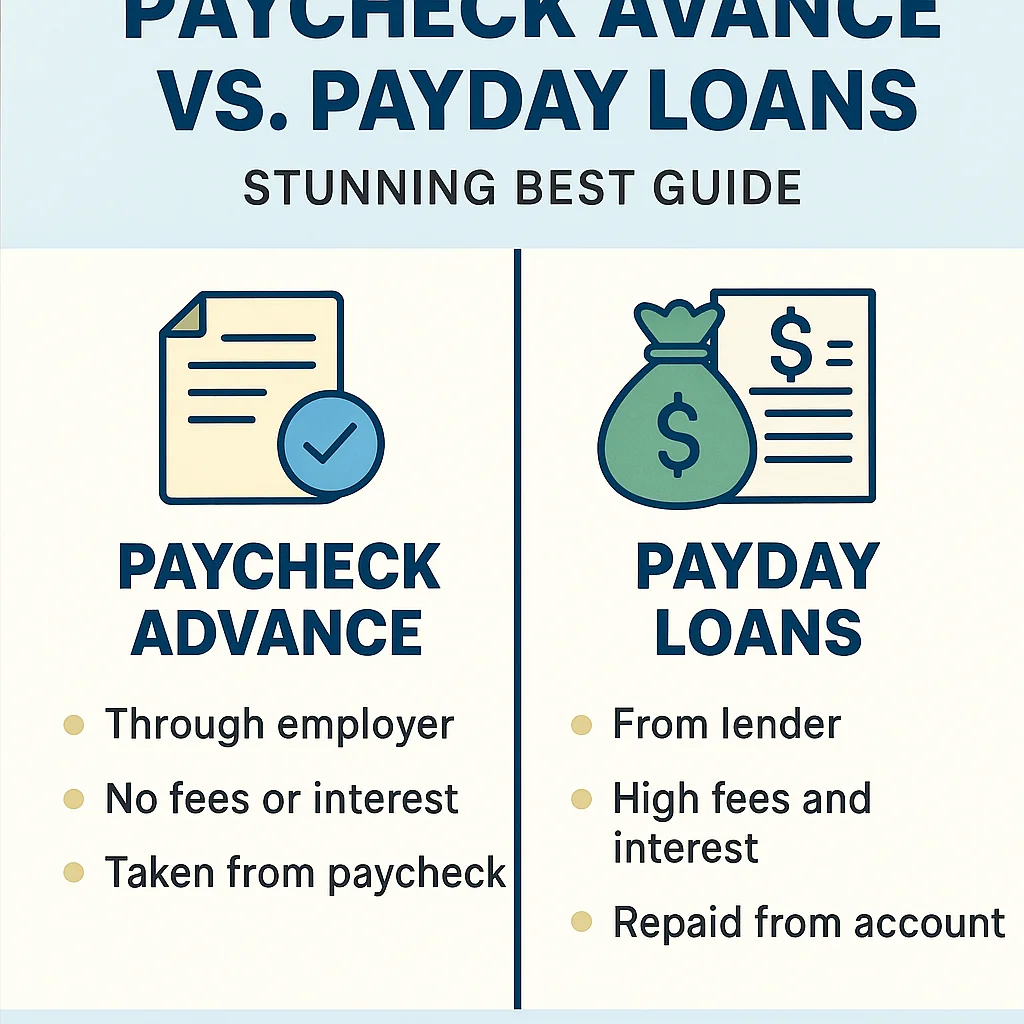

Key Differences Between a Paycheck Advance and a Payday Loan

Both options give fast cash before payday, but they differ in cost, risk, and structure. The table below highlights the most important contrasts.

| Feature | Paycheck Advance | Payday Loan |

|---|---|---|

| Source of money | Your already earned or expected wages | New short-term debt from a lender |

| Typical cost | Free or low flat fee; often no interest | High fees; very high effective APR |

| Repayment method | Automatic deduction from upcoming paycheck | Bank account debit or post-dated check |

| Loan size | Usually capped at part of your paycheck | Based on lender rules, often a set cash amount |

| Main risk | Smaller future paycheck; possible cycle of advances | Debt spiral, high fees, repeated rollovers |

| Credit check | Rare or very light | Often none, but reported in some regions |

In simple terms, a paycheck advance usually gives cheaper access to your own money, while a payday loan sells you expensive borrowed money with more strings attached.

Is a Paycheck Advance Better Than a Payday Loan?

In most cases, yes. A paycheck advance is usually less expensive and less risky than a payday loan because it links to your income and may not charge interest. Still, “better” does not mean harmless, and both options can cause trouble if used often.

Pros and Cons of Paycheck Advances

Paycheck advances solve short-term cash needs, but they also affect the cash you will have next payday. Understanding both sides helps you decide if the trade-off is worth it.

Advantages of Paycheck Advances

Some key strengths stand out for paycheck advances compared to payday loans.

- Lower cost: Many employer programs are free or charge a small flat fee, which is much cheaper than typical payday interest.

- Based on income: Limits often match your earned wages, which can reduce the chance of borrowing far more than you can repay.

- No traditional debt contract: Often no formal loan, so you may avoid hard credit checks or long-term obligations.

For someone who just needs to bridge a few days before salary hits, these benefits can make a paycheck advance the safer short-term choice.

Drawbacks of Paycheck Advances

At the same time, paycheck advances carry real risks if they become a pattern instead of a one-off fix.

- Smaller future paycheck: You get relief now but have less money later, which can restart the same problem next month.

- Dependence cycle: If you lean on advances every pay period, you may never feel “caught up”.

- Fees from repeated use: Even low fees add up if you use the service often.

Frequent dependence on paycheck advances is a signal that income and expenses are out of balance, not just a timing issue.

Risks of Payday Loans

Payday loans often look easy: fast approval, cash in minutes, few questions. The real cost comes later, especially if you cannot repay in full on the due date.

- Very high effective cost: A “small” fee over just two weeks can equal hundreds of percent APR over a year.

- Debt spiral risk: If you roll the loan, each renewal adds more fees and digs the hole deeper.

- Bank account strain: Lenders may attempt multiple withdrawals, causing overdrafts and bank fees.

- Stress and pressure: Aggressive collection calls and constant worry over due dates can affect mental health and relationships.

One missed payment can turn a short-term fix into a long-running debt chain, especially for people with few other options.

When a Paycheck Advance Might Make Sense

Paycheck advances work best for short, rare gaps, not for chronic budget shortages. One clear example is a one-time medical copay or emergency travel ticket that falls a few days before payday.

In that type of case, with a firm plan for repayment, a paycheck advance can be a practical choice compared to high-interest debt.

- You face a one-time, urgent bill.

- You are sure your next paycheck covers both regular bills and the reduced wage.

- You have checked the fee structure and know the total cost.

If you already struggle to pay rent, utilities, or food each month, an advance will not fix the gap; it will just move the shortfall forward.

Smarter Alternatives to Both Options

If you have a little time and access to other tools, you may be able to avoid both paycheck advances and payday loans. The aim is to reduce cost and risk so that one emergency does not turn into long-term debt.

Lower-Cost Options to Consider

Some alternatives require planning, while others can help even in the middle of a cash crunch.

- Overdraft line of credit: Some banks offer this at a lower interest rate than payday loans or repeated overdraft fees.

- Credit card with lower APR: While still debt, a standard credit card often has a much lower rate than a payday loan.

- Personal loan from a bank or credit union: Even a small personal loan with a fixed rate and schedule can be cheaper and safer than payday credit.

- Payment plan: Many clinics, repair shops, and utilities allow staged payments if you ask early.

- Borrowing from family or friends with clear terms: Not ideal, but sometimes less harmful than high-cost lenders if handled with honesty and a written agreement.

These choices require more effort than walking into a payday store, but they can save large amounts of money and stress over time.

How to Reduce Future Reliance on Cash Advances

A one-off paycheck advance in a genuine emergency is common. The real concern starts when you feel pulled to ask for early pay every month. Small, steady changes can reduce that reliance.

Consider this simple sequence:

- Track every expense for one month, even small ones like snacks or rideshares.

- Cut or pause two or three non-essential items and direct that money to a small “emergency buffer”.

- Set a goal to reach at least one week of living costs in savings, then build towards one month.

Even a modest buffer, like $200–$300, can prevent many small emergencies from turning into debt decisions.

Which Should You Choose?

If the choice is strictly between a paycheck advance and a payday loan, a paycheck advance is usually the safer, cheaper option, especially if it comes from your employer or a low-fee app. It deals with timing issues rather than pushing you into high-cost debt.

Still, both options are stopgaps, not long-term fixes. The best outcome is to use them sparingly while building more stable tools: a basic emergency fund, a clear budget, and, where possible, access to lower-cost credit. That shift turns cash shortages from recurring crises into rare events you can handle without extreme borrowing.